![How To Create An Inventory Management Strategy [+5 Techniques]](https://www.extensiv.com/hubfs/Skubana/Blog%20Pages/Imported_Blog_Media/automation-Oct-12-2022-05-50-14-95-PM.jpeg)

There’s really no denying how important inventory management is for any modern ecommerce business. Without effective inventory management, your company runs the risk of frustrating its customers, losing vital sales, or investing in inventory that doesn’t sell. As you can probably imagine, any of these circumstances will be counterproductive to your growth, and can be quite detrimental to your bottom line, as well.

Read on to discover what it takes to develop a successful management strategy, so you can enjoy inventory optimization and greater profits across all sales channels.

5 Inventory Management Techniques

Although there are a wide range of inventory management strategies available, a few methods continue to stand out among the crowd. These five strategies are not only some of the most commonly used, but they’re relatively easy to enforce within an existing warehouse setup.

1. Just-in-time (JIT)

Just-in-time (JIT) inventory management aligns orders from suppliers with applicable production schedules. Using a JIT approach, manufacturers can increase efficiency and decrease waste by receiving goods only as needed. The idea behind JIT systems is to keep as little inventory on hand as possible, meaning you don’t stockpile SKUs or raw materials ‘just in case.’ Instead, you simply reorder products to replace the order quantity you’ve already sold.

When properly implemented, JIT inventory management can help manufacturers and business owners reduce storage costs, avoid excess inventory, and keep their products fresh.

2. First-In, First-Out (FIFO)

First-In, First-Out (FIFO) is a warehousing technique that functions exactly like it sounds. With this type of inventory control, the first items to enter your warehouse are also the first items to leave. A FIFO system is similar to a ‘first come, first served’ mentality, except here, that sentiment relates to a product’s lifecycle.

The thought behind FIFO is fairly straightforward: the products you received first have been held onto the longest, and therefore, they’re the closest to being obsolete or expired. For this reason, goods that have been produced or acquired first are also sold, used, or disposed of first, in order to keep inventory valuation high and prevent stock from becoming unsellable.

Extensiv Order Manager’s inventory system natively delivers a comprehensive view of FIFO costs and shipping fees associated with your daily operations across a multitude of reports, including Inventory Value, Inventory Aging, SKU Profitability and demand planning, among many others.

3. Push strategy

A push strategy in inventory management is one where retailers order inventory, and then do their best to sell the products they have in stock — in other words, they ‘push’ their existing stock toward consumers via advertising or marketing campaigns. This technique relies heavily on forecasting customer demand, as businesses estimate how many units of a specific SKU they’ll need for the coming month, quarter, or year (and then order everything at the same time).

With a push strategy, you only have to order and ship products once within the designated time frame, which can cut down on costs associated with manufacturing those items.

4. Pull strategy

On the flip side of the push strategy, there’s pull inventory management. With this system, shop owners keep stock levels at a minimum; rather than forecasting and preemptively placing orders, a pull strategy determines the lowest acceptable inventory count you can keep in your warehouse. Using these calculations, businesses then restock their shelves based on the items customers have already ordered and/or received.

Following this trajectory helps companies reduce the potential for overstocking products they can’t sell, and saves on warehousing costs since there are less items to store. But keep in mind, for a pull approach to work, you’ll need to assess and replenish inventory fairly often if you hope to avoid stockouts, delayed shipments, and dissatisfied customers.

5. Conventional manufacturing strategy

A conventional (or traditional) manufacturing strategy is where the assembly line is perpetually on. What this means is, when one area of the supply chain completes its work, it delivers the output to the next station regardless of that department’s status. This inventory management strategy is an attempt to keep machinery (and team members) from sitting idle for too long.

Problems can arise, however, if/when bottlenecks occur somewhere along the line. In this situation, employees may end up waiting for the materials they need, or, it’s possible they’ll be overwhelmed by an influx of incoming goods. That’s why certain companies have shifted to only producing a set number of products each period, and then holding on to their reserve for an unexpected surge or shortage.

7 Steps To Create A Successful Inventory Management Strategy

Now that you know the 5 inventory management techniques, let’s take a look at how to create one. With these seven steps in tow, you’ll be well on your way to leveraging all the advantages of a comprehensive inventory strategy.

1. Decide on a storage and processing location for inventory

Choosing the right location for your warehouse is key, especially for larger companies who use multiple warehouses to run their business. Advanced inventory management software can help track product movement in and out of each location, which provides an opportunity to save money by keeping your labor and energy costs relatively low.

When possible, partnering with a warehouse that’s close to your manufacturer or supplier will allow you to stock and ship products much faster than your competitors. Or, if you outsource to a 3PL, you can easily scale your business and then shift focus to more value-added activities.

2. Choose an inventory software program

Intelligent software is a fundamental component of any successful ecommerce business, as these programs allow you to make smart decisions that support your growth. Inventory management systems give you access to vital data that makes it simple to complete forecasting, process orders and returns, oversee multi-warehouse inventory, streamline purchase orders, and even eliminate human errors. With that said, selecting software can get tricky. You’ll need to decide on your budget, and name the specific inventory challenges you face (which will inform the integrations you need). Any software you use has to be able to integrate with the systems your team already relies on.

If you’re looking for a place to start, check out Extensiv Order Manager.

3. Set up a vendor agreement with suppliers

Once you’ve decided which suppliers you want to work with, you’ll need to finalize an agreement regarding your shipping and payment schedule. In addition, you’re wise to set some time aside to discuss your timetables with said suppliers. For example, after you’ve submitted a purchase order, get the supplier to commit to an estimated turnaround time when you can expect to receive that order at your warehouse.

On occasion, you may find a certain product is selling slowly (or not selling at all). This is clearly a bad situation to find yourself in, seeing as you’ll still be paying for those products while they remain on your shelves. It may actually be cheaper for you to return those items to the supplier, but to do so, you’ll also have to have established a returns agreement in advance.

4. Establish a clear-cut process for getting rid of excess inventory

Dead stock — that is, stock that isn’t selling — negatively contributes to your carrying costs. As mentioned above, you can opt to return this excess stock to the supplier if you’ve already agreed on those terms. However, if you don’t have set terms (or if the returns policy has expired), the next best thing might be to donate the stock.

Donating to nonprofit or charitable organizations is a great idea not only because you’ll receive a federal tax deduction, but also because if you gift your excess inventory, you’re preventing the competition from buying it and then relisting it for their own gain.

5. Include your inventory strategy in your business plan

It’s important that everyone involved with your business is kept up to date with your evolving inventory strategy. That’s why you’re strongly encouraged to write your strategy into your business plan, and then clearly communicate everything with your team. From there, be sure to update this strategy (and corresponding business plan) as needed over time.

6. Set a reorder point for new inventory replenishment

No matter if you’re a new business or an established brand, few things are as exciting as selling products and fulfilling orders. And yet, discovering you don't have enough fresh products to replace those you’ve sold can definitely throw a wrench in your workflow.

You might tell yourself this isn’t a problem, and that you’ll put in an order for the missing inventory and be on your way. But unfortunately, you can lose customers in the interim and risk having to say goodbye to some of your long-term and loyal buyers.

Thankfully, you can avoid this issue entirely by setting a reorder point (and keeping some safety stock around, too). Your reorder point should be based on past market demand, average turnaround time, and your lead time, all of which inventory software can report in a snap.

7. Use metrics to improve future forecasting decisions

In the world of ecommerce, the majority of cash is tied up in inventory — which is why your products are often your biggest asset *and* your greatest liability. But when you utilize a few key metrics, you can make better forecasting decisions for your business. And when you make better forecasting decisions, your inventory is less likely to suffer from an overstock or a deficit (both of which can have an unfavorable impact on your bottom line).

The following are the five best metrics to pay attention to, so you can update, control, and optimize your inventory levels with ease.

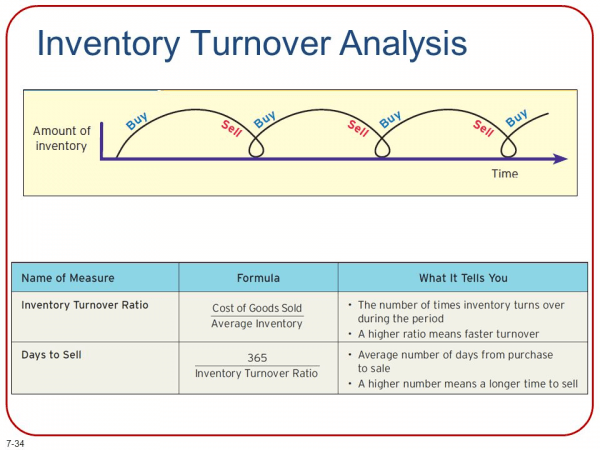

Inventory Turnover

Inventory turnover refers to the number of times a business sells out and replaces its inventory within a specific time period. Typically, inventory turnover is measured by the month, the quarter, or the year. To determine this number, divide the costs of goods with the average inventory; the higher a company’s turnover ratio, the more efficient their operations.

You can use these findings to boost your overall inventory management strategy and aim for a higher inventory turnover. If you shrink your inventory orders, ultimately, you’ll reduce supplier costs and only invest in products where the demand is high.

Gross margin percent

Gross margin is a leading indicator of cashflow as well as profitability, as it can show you how productive your inventory investment really is. To calculate this metric, take your company’s total sales revenue before subtracting the costs of the goods sold. Then, divide that number by the total sales revenue, and you’ll have gross margin percent.

Tracking your gross margin becomes more pivotal as your company scales, because if you can increase your volume, you can also increase your operational efficiency in no time.

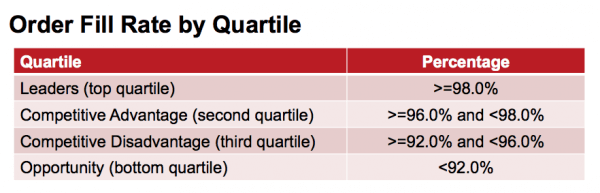

Customer order fill rate

Customer order fill rate measures how well you’re able to meet demand, regardless of unforeseen fluctuations or seasonality. In other words, it’s the percentage of items a customer orders which you were able to accurately fulfill. If your ratio is low, it can indicate your inventory is performing poorly, or perhaps your management strategy isn’t working like you’d hoped.

This particular outcome could lead to a loss of customers, a decrease in sales, and a bad reputation for your brand. In the event you’re unable to meet your customers’ expectations, make sure to communicate with them directly and offer a few viable alternatives.

Costs of carrying

For as long as you keep an inventory, you’ll be subject to carrying (or holding) costs. But just how much does your inventory cost you at any given time? Without assessing this metric, you could be spending a lot more money than is necessary, so it’s in your best interest to calculate and even reevaluate your carrying costs on an ongoing basis.

Average sell out days

Do you know how long it takes to sell through your monthly inventory? Understanding this figure will help you assess whether your inventory management strategy is working. For instance, if the average sell out day is as low as five, you could face a deficit. And if the average is too high, you could have dead stock taking up valuable warehouse space.

It's critical for your company to analyze these sell out findings and move forward with a strategy that works for your unique business needs.

Consequences of a Poor Inventory Management Strategy

While all product-based businesses have an inventory, that doesn’t mean they all have a proper inventory management strategy. Retailers who lack solid inventory management techniques are much more likely to experience difficulties within the supply chain, a reduction in productivity, and lost time and money as a result. The following are just four of the consequences of a poor inventory strategy (or no strategy at all).

1. Overstocking & inefficiency

Without a sufficient inventory management strategy in place, it can be very difficult for businesses to make accurate forecasts regarding what (and when) to reorder, since they don’t know what’s selling versus what’s still sitting in their warehouse. Unfortunately, this scenario can cause some companies to take a gamble on new SKUs — and in turn, create an overstocking issue if customers aren’t interested in the products that are available.

The best way to avoid these unnecessary consequences is to implement stock management solutions that’ll give you clarity around what your customers actually want. Systems like Extensiv Order Manager, which help you understand your product selling patterns, make it easier to streamline and improve inventory management, even across multiple sales channels and warehouses.

2. Understocking

When retailers aren’t quite sure when to reorder, they can easily wind up being in short supply or overstocked. (Hint: neither are ideal outcomes.) If you’re overstocked, you’re left with rising holding costs. And when your products are understocked, your customers won’t be able to purchase what they want from you, meaning they’re prone to take their money elsewhere.

But with a good inventory management system, you’ll have access to data that helps you organize your production schedule so you reorder at *exactly* the right time, every time.

3. Inefficient time management

Whether you’re a small business or a large enterprise, time will always be one of your greatest assets, and therefore, it's important you manage your time well. So then, why lose more than you have to by using a weak management strategy? Successful brands know a skilled inventory management system can save you a significant amount of time. That’s because inventory management software automatically keeps track of your records, so you don’t have to go over them manually to ensure they’re correct.

In addition, relying on quality management solutions means you won’t waste time trying to make forecasts without accurate data, since these programs support ongoing, precise reporting.

4. Increased costs

If your company starts to lose or leak cash, it probably won’t be long before the rest of your operations are similarly affected. One of the primary reasons cashflow becomes impaired is the lack of a solid inventory management system. Without these tools and software solutions, businesses are often unable to take on the costs associated with having an inventory (like space, storage, insurance, and investment costs, to name a few).

The good news is, inventory management programs help businesses cover these costs and provide more working capital, which you can use to improve other areas of your operations.

Key Takeaways

Building the right inventory management strategy is an iterative process that is unique to each business. As we saw, there are a number of factors to consider as you begin developing an inventory management strategy — but after it’s up and running, you’ll be able to lean on inventory management software to automate and improve your process.

Extensiv Order Manager automates functions as a source of truth to manage inventory across multiple channels. Extensiv does this by enabling efficient cost and resource distribution. Not to mention, inventory insights that will inform business decisions that will drive results for your bottom line. Learn more about how you can level up your business with Extensiv Order Manager!

Be the first to know

Subscribe to our newsletter