The retail inventory method is a generally accepted accounting principle that provides an educated estimate as to how much stock remains within a specific accounting period. Some businesses find the retail inventory method to be a helpful resource while they have goods in transit or when they’re working within a time constraint (and are unable to perform precise counts). Though this method has its advantages, there are notable limitations to what it can achieve, as well — which is why so many retailers have gone in search of alternative solutions.

What is the retail inventory method (RIM)?

The retail inventory method (RIM) is an accounting tool that quickly estimates the value of your merchandise. More specifically, the RIM gives an assessment of ending inventory value by measuring the cost of inventory items in relation to the price of said goods. This method makes use of sales data and cost-to-retail ratio to generate its estimates, meaning retailers can gather approximations without having to sort through each of their warehouse shelves.

When to use the retail inventory method

When the merchandise has a consistent mark-up percentage

It’s recommended that sellers only use the retail inventory method when their merchandise has a consistent mark-up percentage. In other words, this technique is reserved for situations where there is an established relationship between (1) the price inventory is purchased, and (2) the selling price for consumers. For example, if a sneaker brand marks up every pair of shoes by 100% of the wholesale price, this consistency would allow for correct use of the RIM.

When you need an approximation on inventory value

It is important to remember the retail inventory method provides estimations, not concrete data. With that in mind, if your store needs an approximation of its inventory value, the RIM could be a choice resource to utilize. The reason these numbers are merely approximations is that select goods within a retail store or warehouse location are likely to have been broken, misplaced, or even shoplifted at some point — which won’t be properly accounted for by this method.

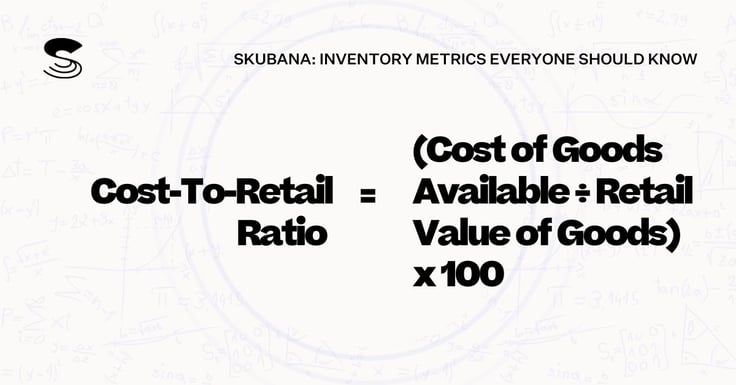

To understand the cost-to-retail ratio

The cost-to-retail ratio looks at the percentage of an item’s suggested retail price that’s made up of costs. This ratio is calculated using the formula: cost-to-retail ratio = [cost of goods available for sale ÷ retail value of goods available for sale] x 100. Understanding this ratio is pretty pivotal, as it informs business owners on the percentage that goods are marked up from the wholesale purchase price to their retail sales price (so they can make adjustments as needed).

How to calculate the retail inventory method

Step 1: Calculate the cost-to-retail percentage

As mentioned above, the cost-to-retail percentage (or ratio) can be calculated as: [cost of goods available for sale ÷ retail value of goods available for sale] x 100. An example of cost-to-retail percentage in action could look like a laptop that costs $600 to manufacture and sells for $1,000. In this case, the cost-to-retail ratio is: [$600 ÷ $1,000] x 100, or 60 percent.

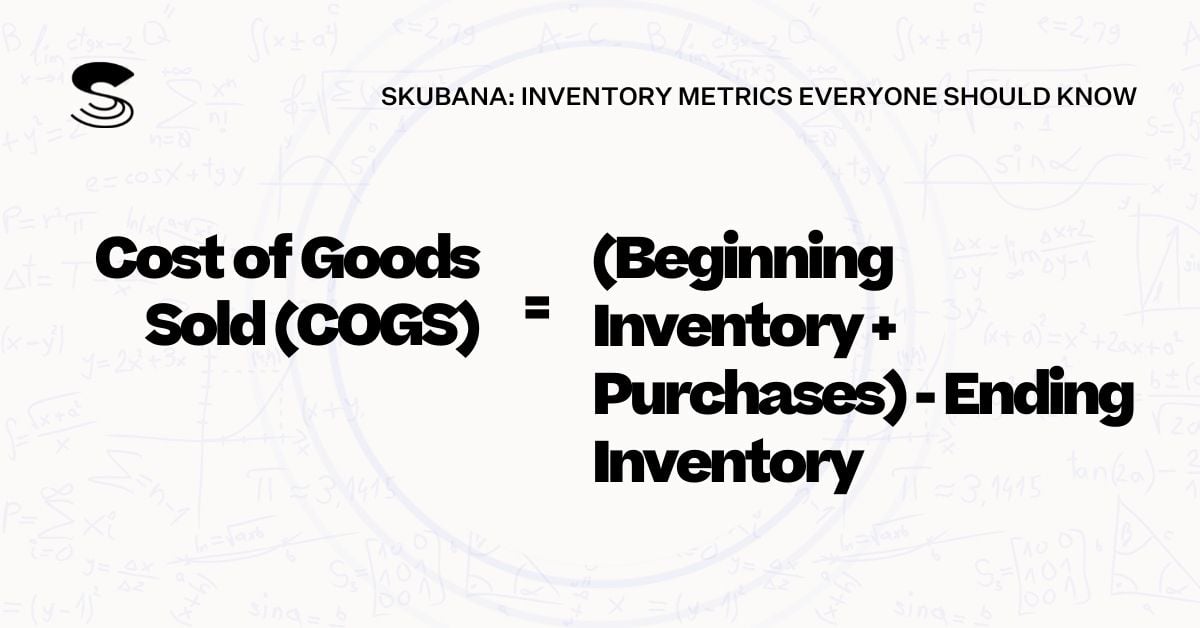

Step 2: Determine cost of goods sold (COGS)

Cost of goods sold (COGS) refers to the price of producing goods that are sold by a brand or business. To calculate your own COGS, apply the formula: cost of goods sold = [beginning inventory + purchases during period] – ending inventory. Here, the beginning inventory is the amount of goods leftover from the previous period (month, quarter, etc); the purchases during period points to the cost of what you purchased within the designated accounting period; and lastly, the ending inventory is whatever didn’t sell during that same timeframe.

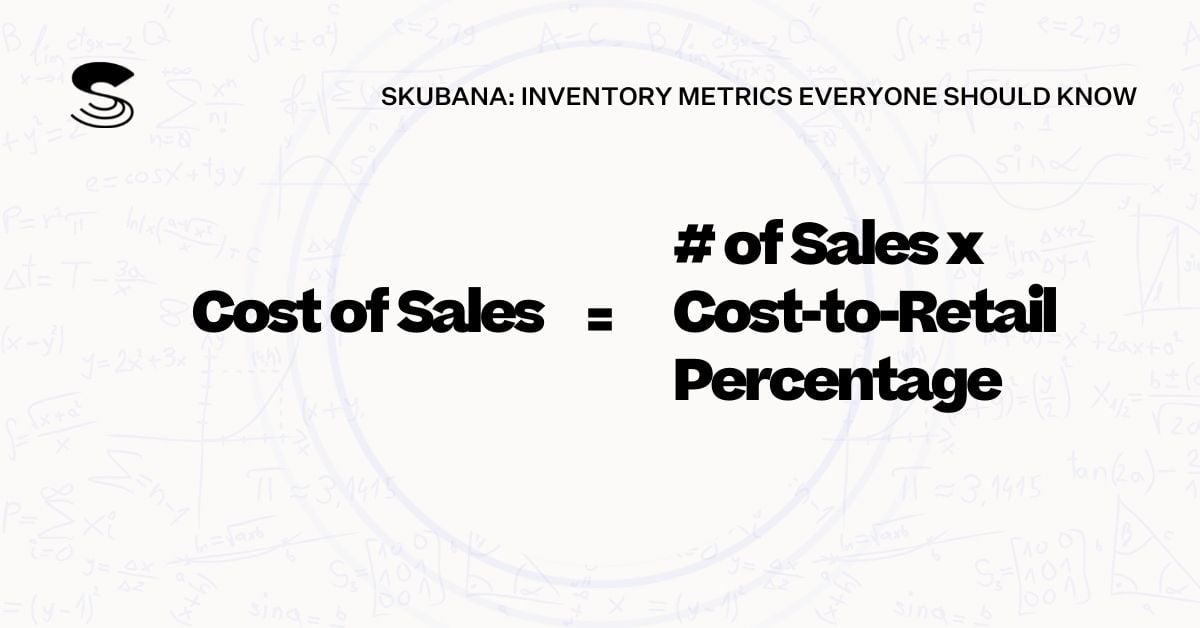

Step 3: Determine cost of sales

To determine the cost of sales for your business, you’ll first need to tally your total sales during the specified period of time. From there, use the formula: cost of sales = [number of sales x cost-to-retail percentage]. Since you’ll have already uncovered your cost-to-retail percentage in Step 1, you can easily apply it again here in Step 3 for even quicker calculations.

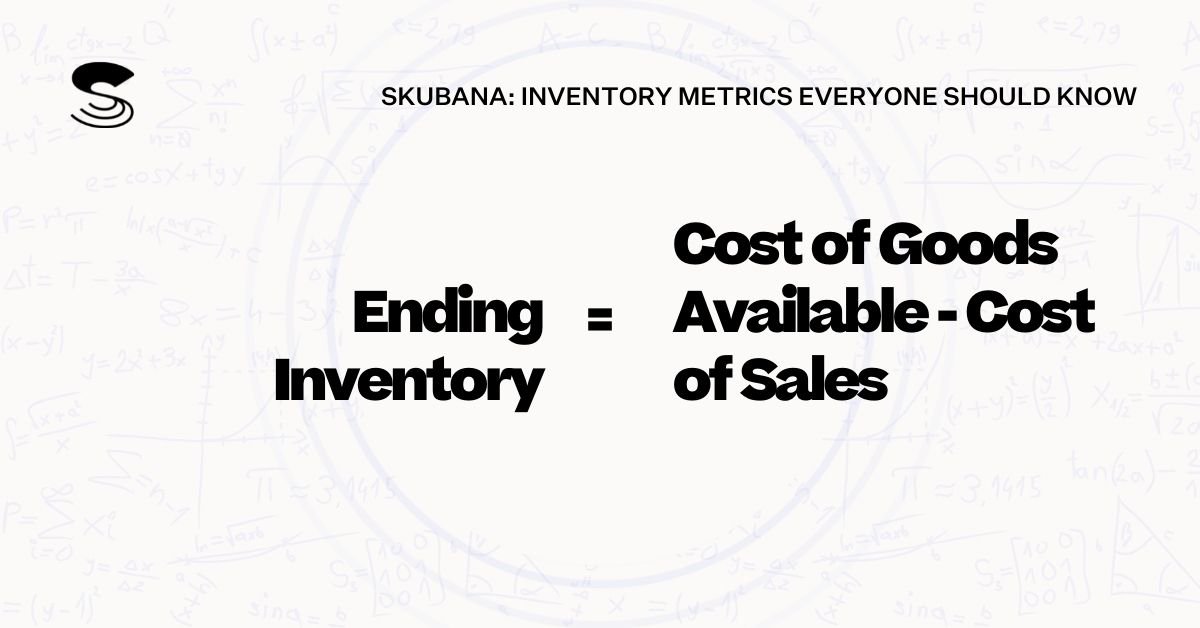

Step 4: Calculate ending inventory value

In order to calculate your ending inventory value, you’ll need to complete the formula: ending inventory = [cost of goods available for sale – cost of sales]. As you can see, the first three steps in this process each play an important, distinct role within the retail inventory method (i.e. ending inventory estimates), so you’re wise to follow the order laid out for you here.

Retail inventory method example

Let’s look at an example of the retail inventory method, based on the laptop numbers used earlier. We already know the cost-to-retail percentage came out to 60%, so now let’s imagine the total laptop sales for the period were $1.5 million, and the following is also true:

Cost of beginning inventory = $800,000

Cost of purchases = $400,000

Cost of goods available for sale = $1,200,000

Total cost of sales = 900,000 [sales of 1,500,000 x 60%]

Ending inventory value = $300,000 [1,200,000 – 900,000]

As you can see, the retail inventory method gave an estimated inventory value of $300,000 for the selling period on your financial statements. This evaluation will be fairly reasonable, so long as the laptops didn’t experience changes in mark-up value (or at-cost pricing).

Pros of the retail inventory method

Quickly estimate retail merchandise value

The retail inventory method is often used by retailers who are short on time, since this is a helpful strategy to estimate their merchandise value on the fly. That’s because the RIM is rooted in simplicity; it’s a quick calculation that offers relevant inventory estimates, which can then be referenced when making certain purchasing or budgeting decisions for your business.

Works for sellers with predictable inventory

Many sellers and wholesalers find the RIM useful when they’re working with predictable inventory items — that is, large volumes of goods with consistent mark-up value. Likewise, some warehouses can take advantage of this method, given that the types of products they store don’t change in value from season to season (or they have a very slow turnover ratio).

Estimating retail goods in transit

The RIM is also a valid accounting method for estimating retail goods in transit. A retail business with multiple stores or warehouse facilities may find it difficult to monitor product movement in (and across) these varied spaces. Fortunately for them, the retail inventory method can estimate goods on the move, thus offering some solid appraisals within the larger inventory picture.

Cons of the retail inventory method

Numbers are just estimates

One of the most substantial drawbacks of the retail inventory method is that the numbers are just estimates, nothing more. And although these estimates might be easy to compute, convenience is not synonymous with accuracy here. For that reason, the RIM should always be supplemented with other inventory valuation methods or a physical inventory count to confirm your results. This way, you can better guarantee the accuracy of critical inventory reporting.

Only reliable for products with consistent mark-ups

While consistent mark-ups sound nice in theory, the reality is, they rarely come to fruition since different mark-ups happen in response to market fluctuations. Because the RIM assumes the previous mark-up percentage will remain true for the current selling period, any changes to this mark-up (i.e. post-holiday markdowns) will cause major inaccuracies in the calculations. This issue is not one to be overlooked, and should instead be met with careful consideration.

Requires accurate demand forecasting to be trusted

Another concern regarding the retail inventory method has to do with demand forecasting. There’s no doubt that inventory forecasting is a valuable part of any inventory management strategy, and yet, many businesses still rely on manual processes to create forecasting reports. Unless demand planning is properly automated, it cannot be trusted to produce accurate predictions (and therefore cannot be trusted to deliver useful estimates via the RIM).

3 reasons to use a retail inventory method alternative

Get accurate, real-time inventory data

As you can see, accuracy is not the retail inventory method’s strong suit; however, accurate inventory calculations are the backbone of a successful product-based brand. When it comes to leveraging real-time inventory data, Extensiv Order Manager (formerly Skubana) uses real data — not static spreadsheets — across all selling channels for consistent, reliable metrics that put manual estimates to shame.

Improve inventory management efficiency

Extensiv brings clarity to everything you do, thanks to a unified and user-friendly platform that simplifies your most complex operational tasks. And when these tedious, time-consuming tasks become streamlined, improved inventory management efficiency is sure to follow. By partnering with Extensiv and utilizing real-time data, you’ll no longer have to double check your inventory estimates by comparing the RIM numbers with your First In, First Out (FIFO) or Last In, First Out (LIFO) inventory counts. Simply put, Extensiv eliminates that doubled workload for good.

Gain inventory insights

Not only does Extensiv Order Manager enhance your operational efficiency, but this system goes a step further by acquiring insights from your inventory data, as well. These insights likely include identifying trends with inventory costs and buying patterns — information that will largely influence the way your business scales. What’s more, by shifting resources from tracking inventory to finding growth opportunities, Extensiv users can set themselves apart from the competition and further increase their profit margins.

Interested in how Extensiv can help your business move beyond the retail inventory method and unlock its operational potential? Consider booking a free demo today!

Be the first to know

Subscribe to our newsletter